Stock Buildup in China……And Now the Russian Ban!

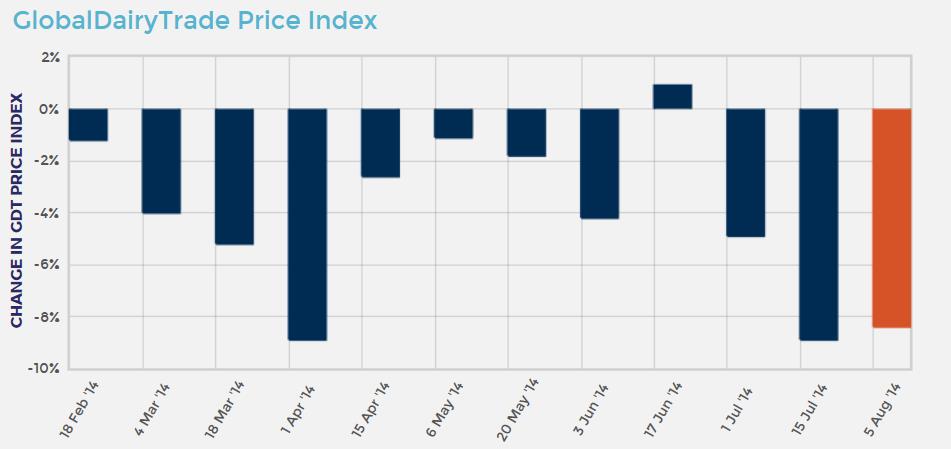

The generally poor sentiment that has re-emerged in dairy markets of late, and has been particularly evident in last Tuesday’s drop of 8.4% in the GDT auction (following on from a drop of 8.9% and 4.9% in the two preceding events), and which had been blamed on strong global supplies and a significant stock build-up in China, now looks like being exacerbated by Russia’s announcement of it’s intention to block EU dairy imports.

The most recent GDT price for whole milk powder, of $2,725, puts milk in the 20c per litre ballpark, and while that price level is almost certainly unsustainable for even the most efficient Kiwi producers, and should be subject to a rebound, it does suggest that the market position for the immediate future will not be positive. Buyers seem to be intent on sitting back in expectation of further price weakness, prompted by strong supply numbers from Europe, the US and New Zealand, and by expected weaker demand from China, given the reports of significant volumes of stock overhanging the market there.

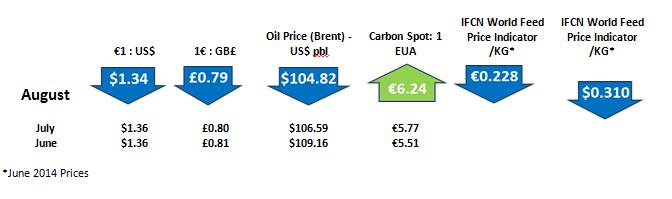

Optimists point to ongoing general demand strength across key markets, coupled with the expectation that moderating prices will improve affordability and prompt buying in developing markets. They also remind us that we are going through an unprecedented period of almost 5% supply growth, and that it is improbable that supplies would continue to grow at such a pace. The Russians will also need to keep sourcing supplies of cheese and butter elsewhere, thereby eating into someone elses stocks. Also, our great rivals in exports, the US, are coming off a milk price base of $21.60 per 100lbs, or around 37c per litre. This means that they won’t be in a position to quickly join the race to the bottom in export markets. Meanwhile the current Eurex index values European at around 33c per litre.

The pessimists suggest that the reduced presence of Russia and China in the market will prompt all other buyers to hold back and watch prices drop still further. The crucial issue will be the degree to which European and US supplies respond to weaker prices. Irish and many European suppliers will also have superlevy concerns, but cheap concentrates, good weather, and lots of quality forage may keep the milk flowing.