Markets Weakening Again

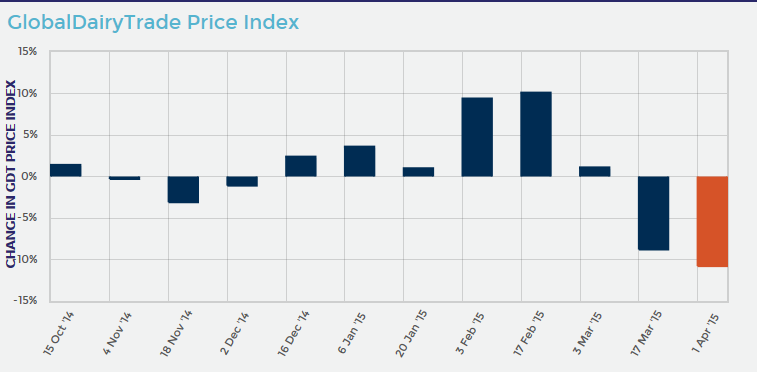

It seemed like the entire dairy sector groaned in unison on April 1st, as news of the latest GDT auction spread. Farmers were breathing a sigh of relief at quota ending, co-ops were dealing with the collection and processing of a massive volume of “held-over” milk, and policy makers were marking the big day with various dairy themed events. The news of the 10.8% Index drop, following an 8.8% drop a fortnight earlier certainly introduced a balanced tone to any celebrations.

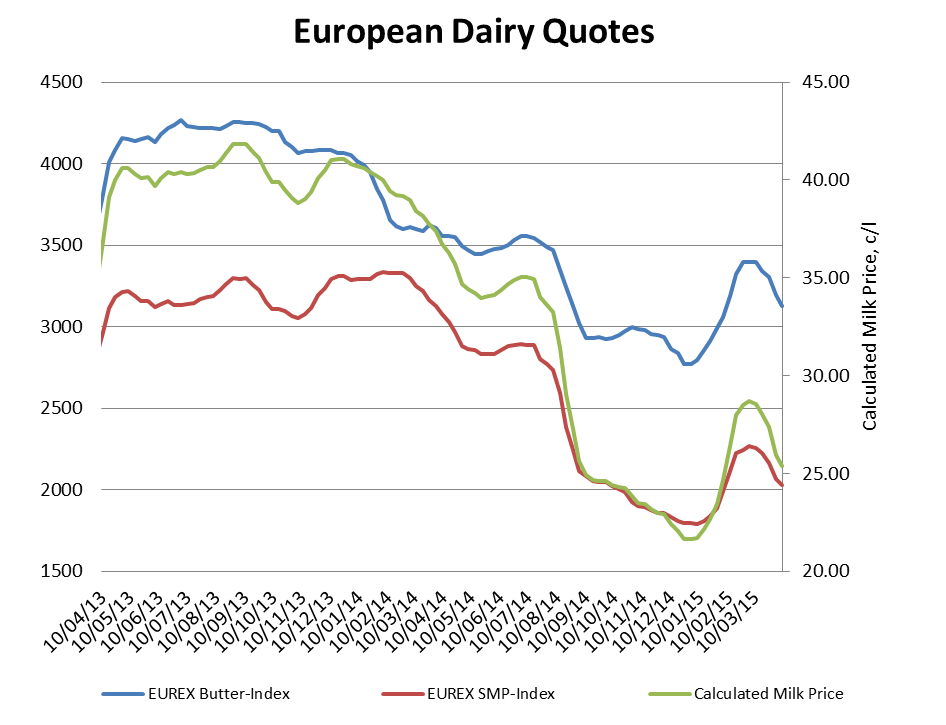

Meanwhile, last week’s eurex butter and SMP indices show a significant, consistent weakening of markets in the past month. The current butter index price, of €3130 is down almost €270 in month, with the SMP index price of €2032 down €235 in the same period. That’s equivalent to 3.3c per litre in milk value lost since early March. Those index prices suggest a milk value of around 26.6c per litre including VAT – significantly lower than the current milk price.

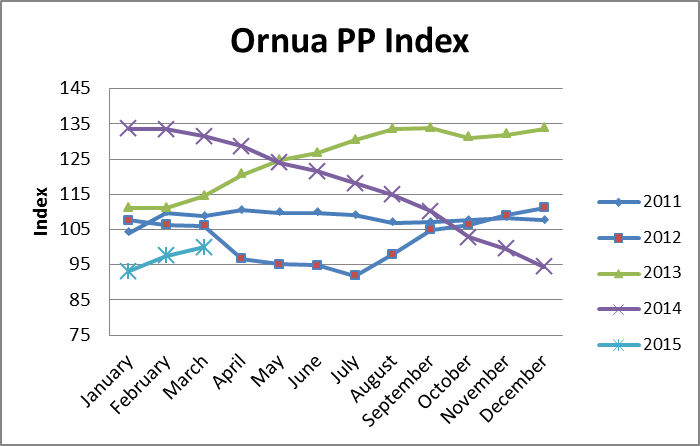

On the positive side, the Ornua PP Index showed growth for March, with the index up from 97.5 to 100. This is reflective of higher butter and cheese returns.

There is no doubt that the current market weakness is due to a combination of buyers expectations of a post-quota flush and significantly greater than expected late season production in New Zealand. The effect of the now since ended “drought” in New Zealand was always over played. This publication highlighted, last month, the fact that soil moisture deficits in New Zealand were nowhere near as serious as in the 2013 drought and indeed, were close to normal levels.

Buyers are now, however, looking at milk flows in Europe and markets will respond to production, or lack of it. The key producing countries of Germany, France, Netherlands and Ireland, as well as the UK, Austria and Poland, will be watched closely. Production in those countries is largely driven by price and weather and we know that milk prices this spring are ranging 30c per litre. The 30c level will not, in itself, drive milk production and it is unlikely to sustain last year’s level of growth (almost 5%) unless growing conditions are exceptional.

Meanwhile, US milk production growth may be moderating somewhat (up by only 1.7% in February, the latest data available). The USDA’s March Livestock, Dairy and Poultry Outlook, still, however, predicts annual growth of 2.47%. The March Class iii milk price of $15.56, is down around $9 in six month, although when expressed in the Euros, it still equates to over 33c per litre (US constituents).