Continued Weakness Through Peak

Despite continued weaker prices and understandable downward pressure on milk supplies, buyers appear to be standing off the market, wondering how the expected wall of milk will give them bountiful supplies of cheap product.

It is becoming clear, now, that the current milk price environment will not drive massive post quota production, and major dairy countries like France and Germany are reducing supplies. While plentiful spring grass is allowing many European suppliers to fulfill their potential, there are expectations that as summer moves on and grass gets scarcer across the continent; farmers will not invest in concentrates to maintain production. It remains to be seen how long it will take buyers to realise this, and to start to take cover for their requirements. In the first instance, however, Europe will need to shift its current high level of SMP stocks. We will be helped by the weak Euro and being competitive on world markets for SMP, Butter, and Cheese.

The Eurex Butter and SMP quotes continue to weaken, with Butter futures contracts now settling at €2960, and SMP contracts being valued at €1862. Converted into milk values, those prices suggest a further 2.3c/l drop in the past month. Meanwhile, peak capacity issues are resulting in extraordinarily cheap distressed milk across Europe, with anecdotes of milk at 10c (and even 6p per litre in the UK!). The European Milk Market Observatory is reporting spot milk at 18c per kg in the Netherlands.

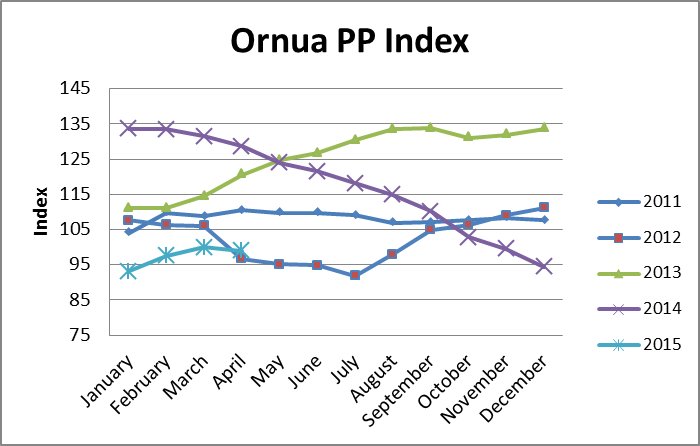

The Ornua PP Index dropped again for April, slipping back to 98.9, from 100 in March, reflecting weaker butter and SMP returns. That index level is suggestive of a milk price of close to 30c. It seems to be a strong vindication of the Irish industry’s investment strategy of late that the PPI, reflective as it is of the wide basket of Ireland’s dairy offering, that it can generate returns well above the traditional commodity butter and SMP markets.

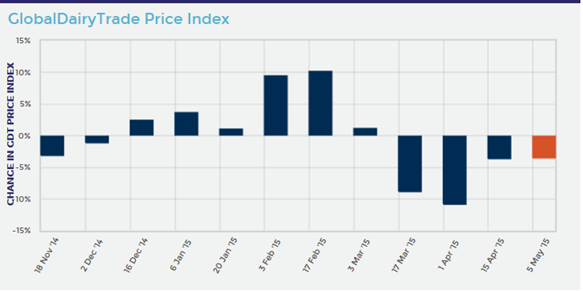

The continued weakness in the GDT auction, with a further 3.5% fall last week, combined with an anticipated pay-out of $4.50 is very worrying for Kiwi farmers. That payout level is the lowest in recent history, with $4.75 having been achieved in 2008/09. There had been pay-outs of below $4 in the 2002-2006 period, but farmers have expanded and become much more highly indebted since then.

By TJ Flanagan