Markets Commentary

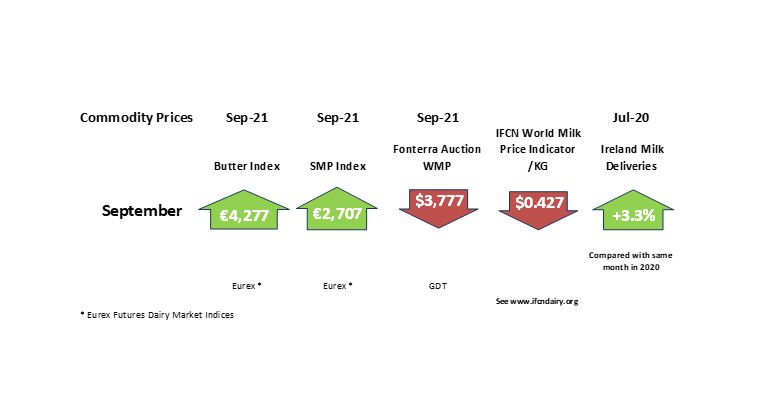

Dairy product prices have firmed, with buyers covering requirements to year-end, following a lull over the summer months.

Global milk supply is still expected to increase by +1.5% year on year. However, milk output has eased especially in the EU with German, French, Polish and Dutch flows impacted by rising input costs and dry weather in July.

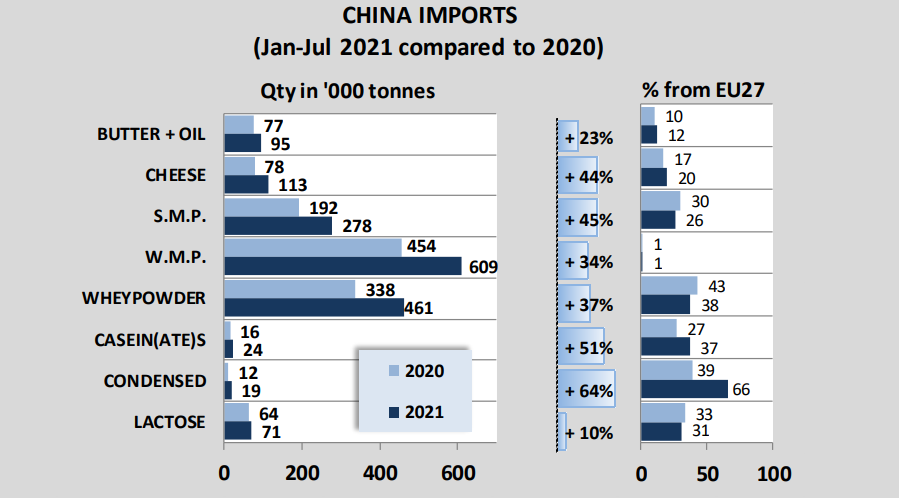

Retail demand remains strong, with the pick up in foodservice slower than expected due to the Delta variant, as economies re-open. The US is the exception with foodservice demand returning to pre-pandemic levels. Chinese buying in July was at elevated levels and future demand from the region will be monitored carefully.

Global supply chain challenges remain such as container availability and a growing issue in the UK related to the availability of lorry drivers. The emerging energy crisis will have an impact on input costs with fertiliser prices at a 5-year high, and while brent is at $70/barrel, oil prices may increase.