Waiting for the Supply Correction

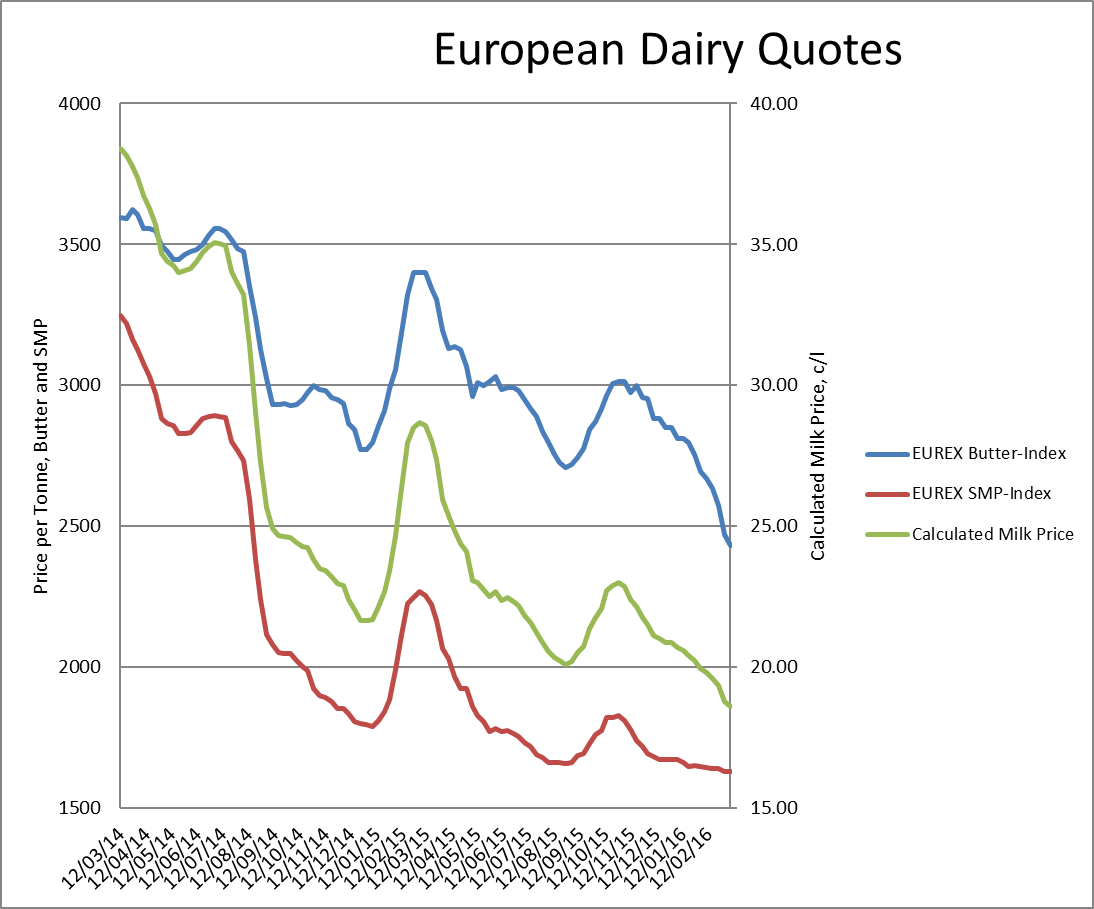

It looks like we’ll need to see evidence of a significant supply reduction before markets begin to turn from their current weakness. Current EEX commodity indices of €2430 for butter and €1630 for SMP are suggestive of milk values well below 20c. Against all expectations, European milk supplies remained strong across the winter and is currently growing strongly again. This is leading to significant discounting of spot milk supplies, which allows traders to get their hands on cheap finished product, further weakening markets.

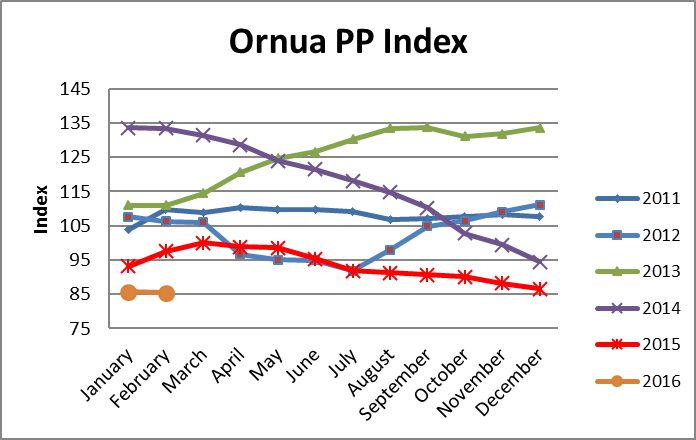

The February Ornua Purchase Price Index dropped slightly to 85.4 from 85.7 in January, another record low, but significantly outperforming all other price indicators.

There is no doubt that a supply reduction will come eventually, either through the supply control schemes to be proposed at the Ag Council meeting on Monday, or through farmers having had enough of low prices. European milk supplies increased by 2.5% in 2015, a not unreasonable figure in the context of quota elimination, but the fact that it came on top of a 3.8% increase in 2014 is the worry. That supply increase resulted in an 8.1% increase in European SMP production and a 4.7% increase in butter volumes. This has resulted in 54,000 tonnes of SMP in intervention already, with the expectation that the 109,000 tonnes threshold will be exceeded within a month. Butter may also soon be offered into intervention.

Meanwhile the latest GDT auction showed a modest increase of 1.4%. The WMP price rose by 5.5% to $1974, roughly equivalent to 17c per litre for milk of standard Irish solids. Last week Fonterra reduced their forecast for the current season to $3.90 per kg, a 13-year low, which is predicted to tip most Kiwi dairy enterprises into severe loss making situations, with consequent financial, social, and personal effects. Kiwi milk supplies, however, haven’t being reducing as much as expected, with a 2.7% drop for the first half of the season, and only 2% in January. This is against a backdrop of a predicted drop of over 5% and an El Nino that didn’t show.