Market Commentary

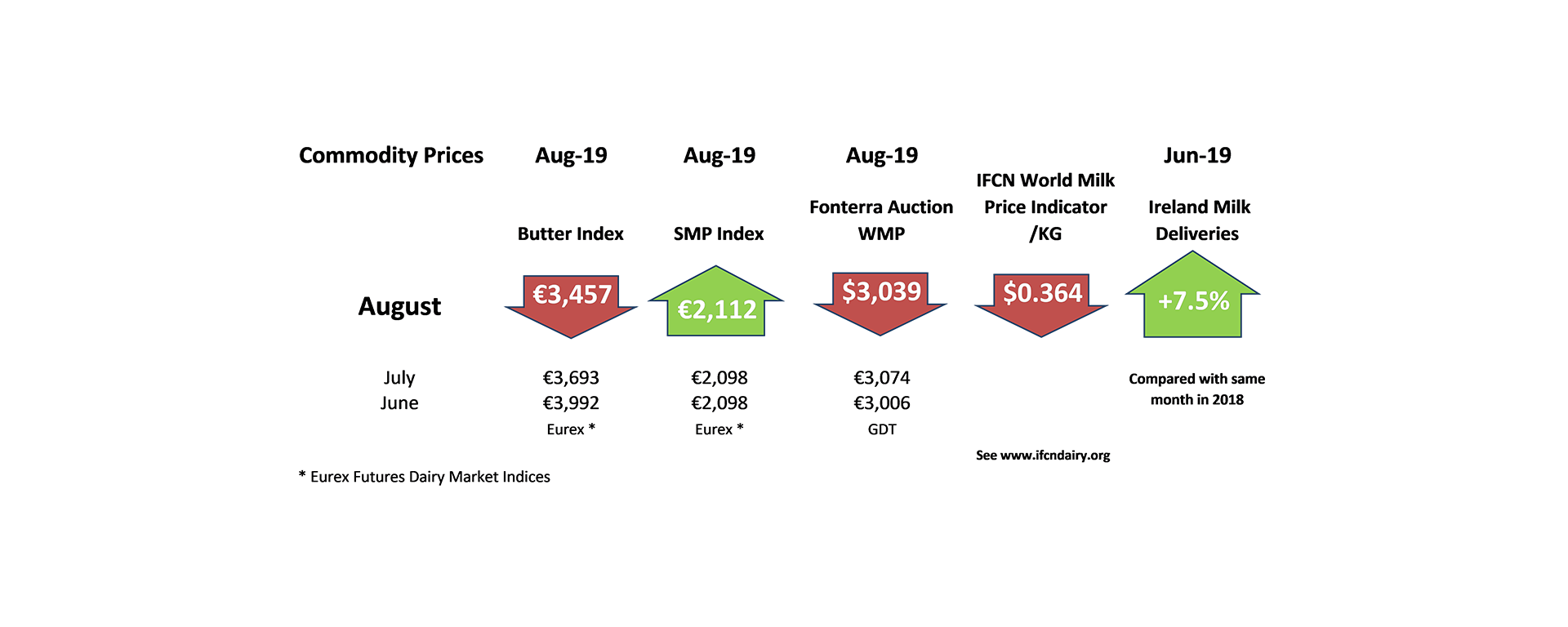

Global milk supply in June fell by -0.4% with EU flows remaining strong in Ireland, the UK and Poland but flows were weaker in Germany, France and the Netherlands. The European Commission is forecasting that milk output will grow by +0.9% in 2019, which will require milk supply to pick up in H2. Milk collections in the US remain static with higher feed prices impacting. Milk flows in New Zealand were strong in June, albeit at a low level of supply.

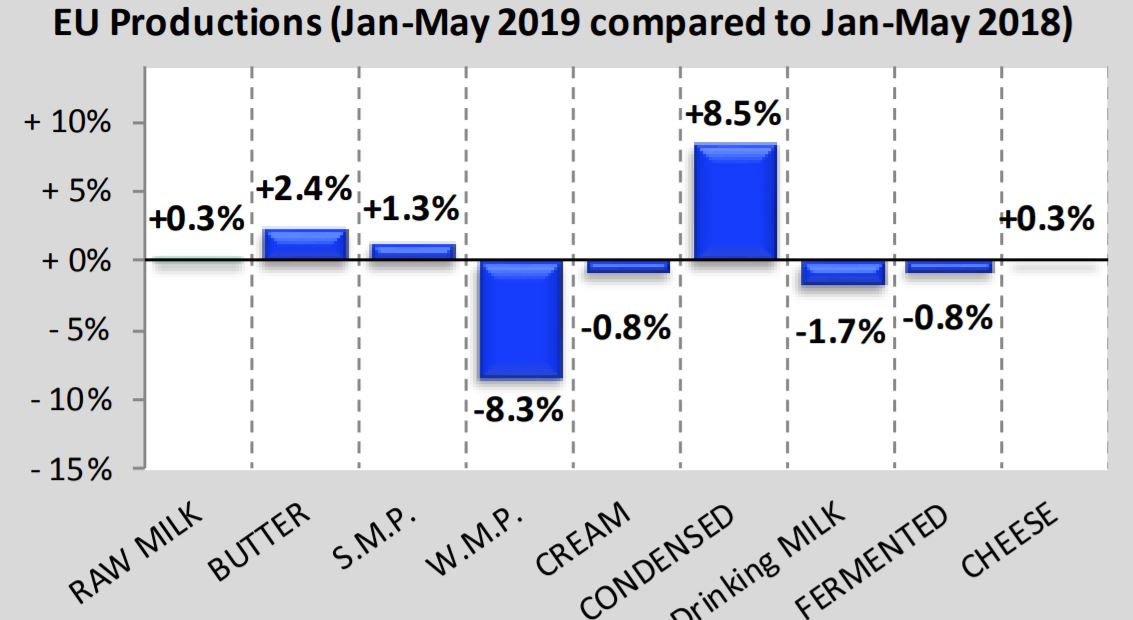

The EEX Butter Index is €3,457 / tonne, a decline of nearly €1000/tonne since the start of 2019, with stock levels higher than demand. EU butter production has increased by +2.4% year to date. The EEX SMP Index is at €2,122 / tonne, remaining relatively flat. Cheese returns are impacted by the weakness of Sterling, as Brexit uncertainty will continue for the foreseeable future.

The continued deterioration in US-China relations is affecting global economic growth and oil demand. Brexit and global trade wars are a major concern for dairy markets, as external trade disputes such as the EU-US aerospace and EU-Indonesia palm oil issues are likely to have wider consequences.