Market Commentary

Global growth in milk supply remains modest with recovery evident in the US and Europe, while milk flows are more restricted in Australia and South America.

EU output increased by +0.9% in September, while US flows were +1.3% in September. In Oceania, Australian output decreased by -4.8% in September, while NZ flows were -0.7%, but up on a milk solids basis. Overall, the rate of global growth is not expected to exceed +0.7% in 2019.

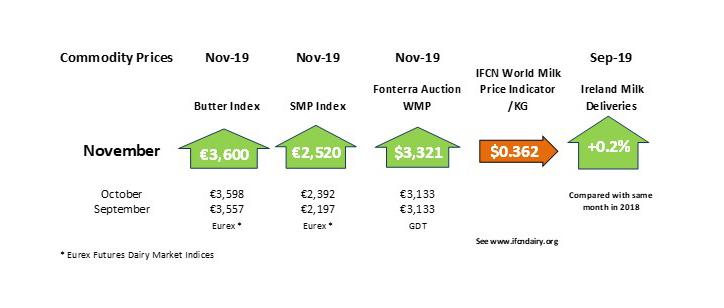

EU butter production is up +3.9% year to date, with the Dutch quotation at €3,550/tonne. Butter production is likely to remain strong due to the recovery in SMP prices. The SMP EEX Index is trading at €2,520/tonne. Delivered prices on the physical market are slighly lower for butter and SMP. Cheese prices are stable but behind alternatives with the Trigona price at €3,125/tonne.

EU Output and Production – Year to Date:

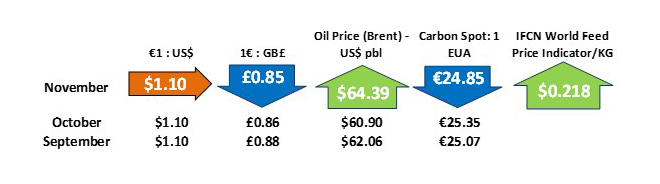

Overall, there remains considerable uncertainty in global dairy markets due to Brexit (although the further extension to the end of January has eased immediate fears of a no deal outcome), US-China trade wars and US traiffs imposed on EU dairy. The strong US dollar and increased protein demand due to ASF will present opportunities.