Market Commentary

The outlook is not as pessimistic but remains challenged, as the food service sector begins to reopen, albeit slowly and normality is returning to China. A prolonged recovery rather than a V shaped recovery is a more realistic possibility, as the fall in FS continues to be greater than the pick up in retail demand.

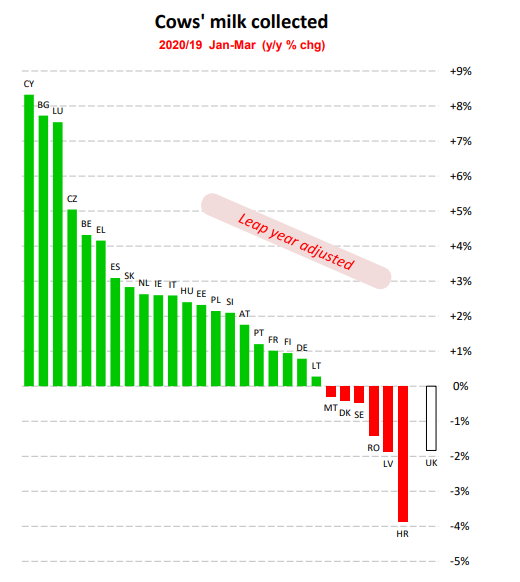

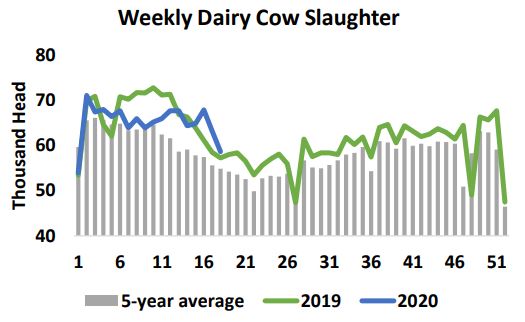

Extremely dry weather in Europe may impact supply, but overall global supply is ahead year to date. EU milk output is +1.7% in Q1 (adjusted for the leap year). US milk output is up 1.5% year on year in April, despite reports of culling and reduced feeding.

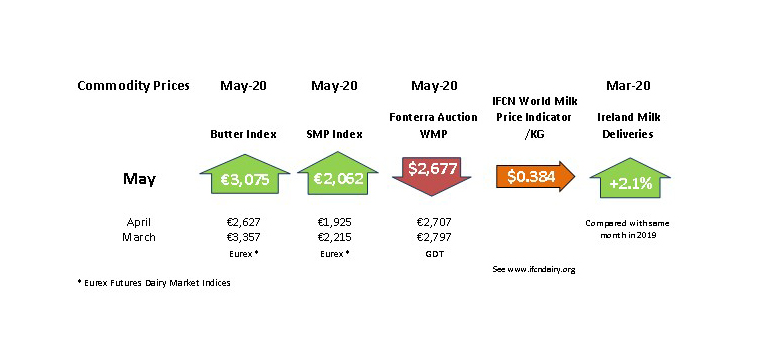

Direct aid provided to US farmers for Q1 output, capped at €250,000 per individual may slow the contraction in the US dairy herd. Fonterra’s milk price range for 2020/21 is $5.40 to $6.90 per kg MS. The wider range reflects increased uncertainty. The 2019/20 payout is narrowed to €7.20 per kg MS. The EEX Butter Index has picked up over recent weeks, with the Dutch quotation up at €2,980 / tonne, with butter benefiting from the opening of PSA and fears concerning intervention have abated. The SMP Index stable at €2,062 / tonne.

Eamonn Farrell – Agri Food Policy Executive