Market Commentary

Dairy markets are generally positive with global supply described as modest and demand remaining solid.

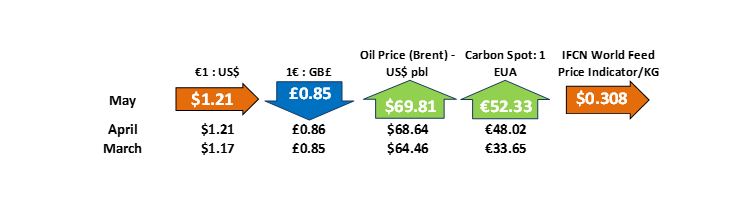

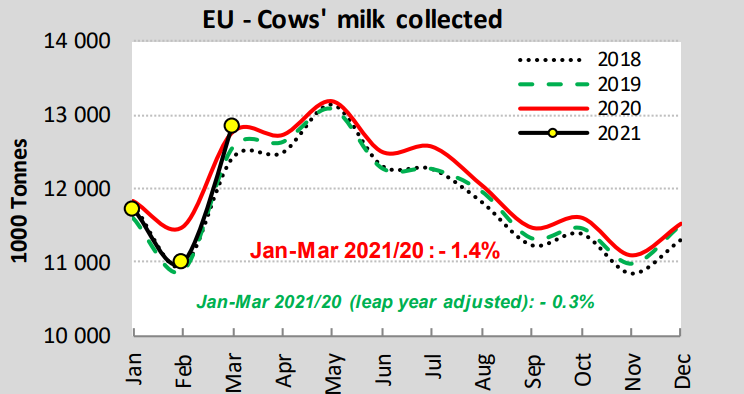

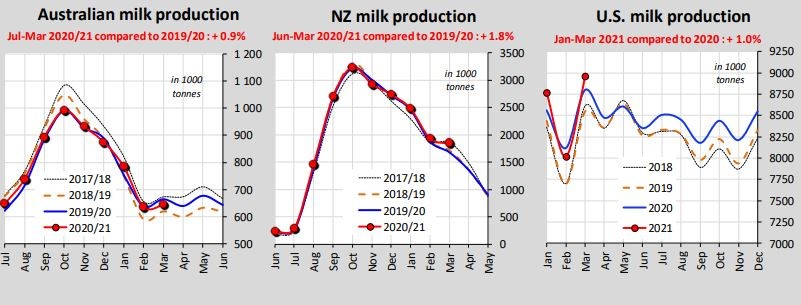

Global supply is predicated to be between +1% and +1.2% in 2021. Output in the USA remains strong (+1.8% in March y-o-y) and supply is forecast to grow into 2022. Milk collection is up year on year in New Zealand, with Fonterra announcing a record opening milk forecast price for the 2021/22 season. EU milk supplies are curtailed by sluggish output in Germany and France, but Irish output is strong through the peak production months. The unseasonably cold weather and rising feed costs are factors in the EU.

EU Milk Collection

Global Milk Collection

There are some signs of volatility but overall, the outlook ahead is stable. The COVID-19 pandemic has had a dramatic impact on the dairy sector, with the restrictions and lockdowns, ultimately proving positive for dairy demand and consumption. The food service sector is now tentatively showing signs of recovery in certain markets, which is another plus.

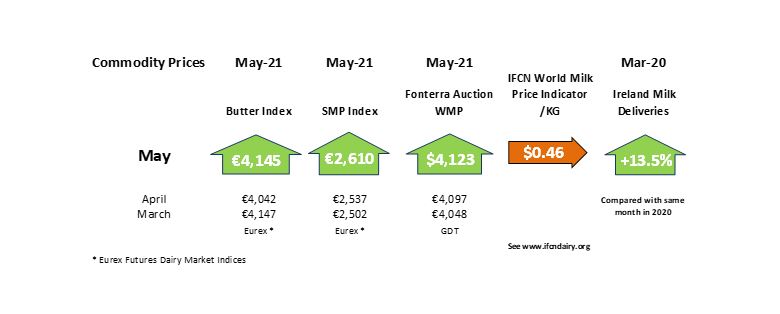

The EEX Butter Index is €4,145 / tonne with the Dutch quotation slightly lower. The SMP index is €2,610/tonne. SMP prices are firmer, supported by continued strong demand from China, as their consumers opt for healthier nutrition options such as dairy following the pandemic. Cheddar prices remain stable supported by strong retail demand.