Market Commentary

The current situation is very challenging for dairy markets. It is six months since the first reported case of coronavirus in Ireland and now globally there are over 25 million cases worldwide and over 850,000 reported deaths. There is no doubt that coronavirus continues to wreak havoc.

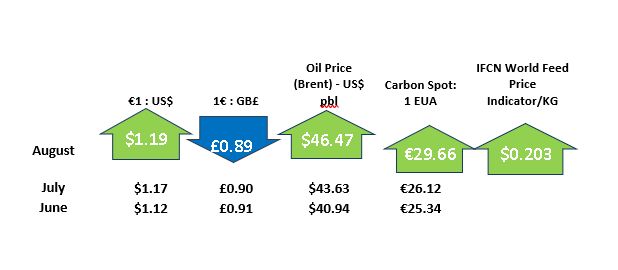

The bleak economic outlook, coupled with high rates of coronavirus in key importing regions are of most concern. Milk supply is expected to increase by +1.3% in H2 (EU milk supply is +1.9% y-t-d, while July output in NZ is +4.4% and in the USA output in July increased by +1.5%). Furthermore, the foodservice (FS) sector is likely to remain extremely fragile, as economies emerge from lockdown and begin to live alongside the virus. Chinese and SEA demand for dairy products is solid, which has supported the market. Government support packages have helped the market, especially in the US but there is a time limit on these interventions. The strengthening EUR has helped the competitiveness of US and NZ exports. Additionally, the purchasing power of the oil exporting countries has been affected by the economic impact of Covid-19.

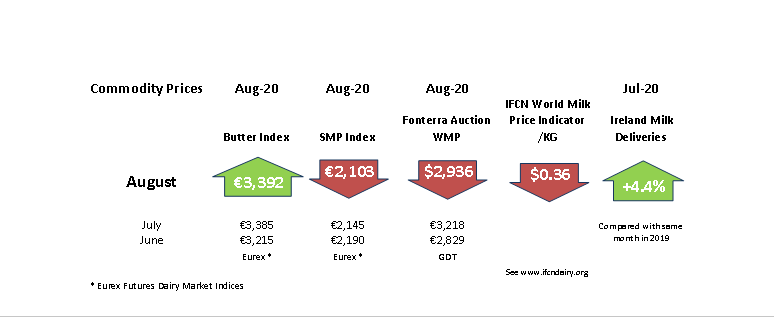

The EEX Butter Index has remained stable during the August period with the Dutch quotation at €3350/t. The SMP Index is lower at €2,103/t. Cheese prices have remained resilient, supported by retail demand but a recovery in FS demand is required.